Core point of view:

More and more evidence at the macro and micro level recently shows signs of a new cycle: industry concentration, corporate balance sheet repair, capacity utilization improvement, commodity prices remain high and long-term ups and downs, corporate financing demand picks up, and the RMB exchange rate strengthens The stock market has come out of a structural bull market.

The stock market is always reborn in despair, rising in controversy, crashing in carnival, and what is the economic cycle? For thousands of years, science and technology and social organizations in human society have made great progress, but human nature has remained unchanged.

The reason why the new cycle has caused such a big discussion is nothing more than two reasons: First, after more than six years of economic recession, people’s inertia thinking has caused , while ignoring the tremendous changes in the microcosm and the cycle of the economic cycle; Most of the arguments against the new cycle are this year's economic and stock market shorts, and we are the minority - the economy and the stock market bulls, the market is the only criterion to test the logic of the view, this year the stock market structural bull market, the economy on the demand side L -type resilience Strong, on the supply side clearing expectations, commodity prices rose and rose, this discussion is finally handed over to the market to test, the market is the fairest referee.

It is expected that this new cycle discussion will be based on solid evidence, solid logic and rational deduction. It is expected that this discussion will promote research progress based on a paradigm of norms and a common context.

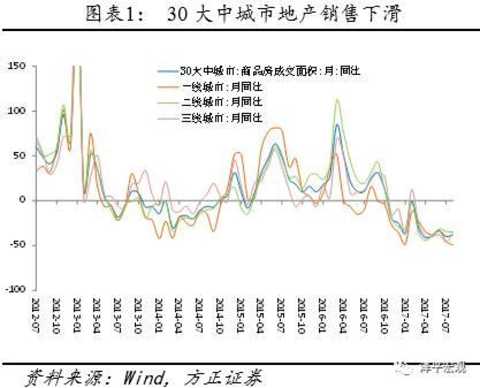

Downstream real estate sales have seen a sharp increase in land supply, and the real estate market has replenished. This week, 30-year real estate sales decreased slightly to -37.9% year-on-year, up 1.9 percentage points from July, but real estate sales in first-tier cities increased by 4 percentage points year-on-quarter to -49.5%. In the first three weeks of August, the national land supply increased sharply year-on-year. Especially in first-tier cities, land supply rose to 99.5% from -0.1% in July. In August, the auto market started stronger, and then the growth rate slowed down. The retail sales growth rate was 4.3% in August, and the first three weeks were 14%, 1% and 2% respectively. The sales of new energy vehicles were hot and sales increased year-on-year. 55.6%; demand for textiles continued to weaken; in July, the export volume of major appliances rose and fell; the freight rate index slowed down year-on-year, the international freight rate increased, and the BDI index increased.

The coal consumption in power generation in the middle reaches increased, and the price of steel has strengthened. In August, the average daily coal consumption of the six major power generation groups increased by 12.4% year-on-year, higher than 10.6% in July. The operating rate of blast furnaces in China fell slightly last week. As of August 10, the daily crude steel output increased by 6.0% year-on-year, lower than the 6.7% year-on-year in July. August rebar prices rose by 60.9% year-on-year, up from 58.3% in July. Supply compression, the peak season is coming, steel is expected to heat up in the future. Cement prices rose 0.2% qoq this week. Cement prices in August increased by 27.0% year-on-year, down from 31.7% in July. Last week, the national cement storage capacity reached 66.0%, lower than the previous value of 66.6%. The chemical product market is generally stable. The global central bank's annual meeting is about to strike, the market remains cautious, and the US dollar index is falling again. The OPEC production reduction agreement may face a threat of rupture, causing concerns about oversupply in the market, and crude oil prices continue to be weak. Supply-side capacity clean-up has gradually landed, and factors such as limited production expectations and declining inventories have led to a rise in non-ferrous prices.

The price of vegetables fell back and the price of pigs rose. Both long and short-term interest rates rose. In August, the price of fresh vegetables fell, and the price of pork narrowed down year-on-year. The National Development and Reform Commission warned that the supply of pork in the second half of the year may increase further. The overall price of pigs will still decline, and the growth rate of Chinese herbal medicines and refined oil products will slow down. The direction of the open market operation this week is mainly reflected in the “sharp peakâ€. The net withdrawal of funds for four consecutive days, the funds are stable and tight, and the net withdrawal funds for Monday, 2, 3 and 4 are 50 billion yuan respectively, 10 billion yuan, 400 100 million yuan, 100 billion yuan. The long-awaited special government bonds have been renewed, and the 600 billion yuan special government bonds issued by the financial institutions through the bond secondary market have been released. The issuance model once again shows the central bank's stable and neutral monetary policy. The R007 interest rate this week was 3.8028%, up 27.54 BP from last week. The DR007 rate was 2.9104%, up 3.91 BP from last week. The one-year government bond yield was 3.3355%, down 0.18 BP from last week; the 10-year government bond yield was 3.6152%, up 2.01 BP from last week. The US dollar index fell and the RMB exchange rate rose.

Risk warning: Fed rate hike exceeds expectations; domestic currency tightening and financial deleverage exceed expectations; real estate regulation is too tight; reform is lower than expected; debt risk

text:

1, Downstream: for increasing, strong passenger car sales

Real estate sales in 30 large and medium-sized cities fell by 1.26% this week. As of August 23, real estate sales in 30 large and medium-sized cities were -37.9% year-on-year, down from -36.7% last year, but higher than -39.8% in July; among them, first- and third-tier cities were -49.5% and -34.8 respectively. % and -36.2%, respectively, below, below and above July -45.5%, -34.3% and -46.0%. The land transaction area in the first three weeks of August fell year-on-year. In August, the turnover of land in large and medium-sized cities was -15.5% year-on-year, down from 0.9% in July, with the first-line increase from -41.2% in July to 8.6%; the second-line fell to -28.6% from 7.7% in July; The third-line fell to -2.0% from 1.6% in July. The year-on-year decline in land transaction area was mainly due to the decline in land acquisition in second-tier cities. In the first three weeks of August, the land supply of 100 large and medium-sized cities increased by 39.9% year-on-year, which was significantly higher than that of July--11.7%. The year-on-year growth rates of land supply in first- and third-tier cities were 99.5%, 38.6% and 37.4%, respectively. July -0.1%, -15.4% and 22.6%.

In August, the car market started stronger, and then the growth rate slowed down. In terms of retail sales, the growth rate in August this year was about 4.3%. The growth rate in the first three weeks was 14%, 1% and 2% respectively, and the growth rate of retail sales slowed down noticeably. In terms of wholesale, the cumulative growth rate in the first three weeks was 10%. Due to too many manufacturers in the first two weeks of August, wholesale sales also slowed down. In addition, according to the latest data released last week by the National Federation of Passengers, the total output of narrow-seat passenger cars decreased by 4.6% in July and 2% year-on-year. The overall situation of the automobile market was good. In July, the production and sales volume of new energy vehicles increased by 55.2% and 55.6% respectively, higher than the 44.4% and 34.1% in June. The new energy vehicles are currently the core development focus of the vehicle enterprises. Guideline for the healthy development of passenger car rental, sharing the legal status of the car in China, which will promote the popularization of new energy vehicles.

Last week, the box office receipts dropped by 31.4%, and the number of people watching and screenings was -28.9% and 2.5%, respectively. Although "War Wolf 2" was the first in the box office for four consecutive weeks, the heat continued to fade. Compared with the same period of last year, the box office receipts and movie attendances in August were 113.3% and 98.2%, respectively, significantly higher than the 6.4 and 2.6% in July. The main reason was the phenomenon-level film "Wolf Wolf 2". Since the release, the box office has continuously refreshed domestic movies. At the box office record, the total box office has exceeded 5 billion. The number of screenings in August was 22.9% year-on-year, slightly higher than 22.0% in July.

The year-on-year growth rate of textile raw materials continued to slow down. The yarn price index in China's textile economic information index this week was unchanged from last week, 5.7% in August, down from 8.4% in July. The price index on grey cloths was unchanged from last week, compared with 1.4% in August, down from 3.6% in July. In the Keqiao Textile Price Index, raw materials, grey cloths, apparel fabrics and home textiles increased by 0.01%, decreased by 0.04%, decreased by 0.57%, and decreased by 0.23%, respectively, which were lower than last week's -0.13%, 1.61%, 0.31% and 0.44%.

According to the latest data released, the export volume of major appliances in July was mixed. Data show that in July China's air-conditioning exports increased by 7.2% year-on-year, and the cumulative increase from January to July was 10.5%. In July, refrigerator exports increased by 10.3% year-on-year, and accumulated from January to July increased by 13% year-on-year. In July, the export of washing machines increased by 7.3% year-on-year; the cumulative exports from January to July increased by 3.7%. In July, color TV exports fell by 10% year-on-year; from January to July, cumulative exports fell by 6.7%.

The container freight index decreased on a month-on-month basis, slowing down year-on-year, and the dry bulk index BDI continued to rise. Last week, the Shanghai Export Container Freight Index (SCFI) fell by 2.1% from the previous month to 40.1% in August, up from 26.4% in July. China's export container freight index (CCFI) fell by 0.3% month-on-month, compared with 21.7% in August, down from 28.2% in July. This week, the Baltic Dry Index (BDI) increased by 3.15% from the previous month, up 66.6% year-on-year, higher than July's 28.1%. Last week, China's coastal dry bulk freight index (CCBFI) fell by 1.1% month-on-month, compared with 11.12% in August, down from 19.9% ​​in July.

2 , the middle reaches: power generation coal consumption increased, steel non-ferrous prices rose

Power generation coal consumption increased this year. The average daily coal consumption of the six major power generation groups increased by 0.3% from the previous month, which was 0.4 percentage points lower than the previous value. As of August 24, the 6 largest power generation groups in this month consumed 802,000 tons of coal per day, up from 721,000 tons in July. The coal consumption of power generation in August increased by 12.4% year-on-year, higher than the 10.6% year-on-year in July. Since August, the temperature has decreased in all parts of the country, and the correlation between electricity consumption and industrial production has been further strengthened. The rise in steel and non-ferrous metals has driven the smelting and production of related enterprises and increased industrial electricity consumption. Uneven rainfall has caused hydropower production to decline and increase coal consumption.

The profit ratio of domestic steel mills has been flat at 85.89% for five consecutive weeks, the highest since April 2017. Last week, the national blast furnace operating rate was 77.4%, a decrease of 0.1 percentage points from the previous month. The increase in blast furnace start-up was mainly due to the increase in the blast furnace start-up of small and medium-sized steel enterprises and the resumption of blast furnace recovery in the previous period. As of August 10, daily crude steel output increased by 6.0% year-on-year, lower than July's 6.7% year-on-year, higher than June's 3.4%. As steel demand enters the peak season and supply is compressed, the market is expected to heat up. Rebar prices rose slightly this week, with the average price rising by 1.7%. August rebar prices rose by 60.9% year-on-year, up from 58.3% in July, mainly due to supply-side reforms.

The national cement price growth rate has slowed down. Cement prices rose 0.2% on a week-to-quarter basis, up 27.0% year-on-year in August, down from 31.7% in July. The off-season of cement is gradually coming to an end, but the demand for cement is generally restored due to the effects of high temperatures, intermittent rainfall and environmental inspection teams. Last week, the national cement storage capacity reached 66.0%, lower than the previous value of 66.6%. Since the middle and late August, the cement price has shown a stable upward trend. The autumn has passed, the cement off-season is coming to an end, and the cement season is the traditional peak season from September to November. The downstream demand is strong and the clinker supply is tight. According to the peak production requirements, the production capacity will be greatly reduced by large-scale shutdown of kiln on November 15. Under multiple benefits, cement prices are expected to enter the autumn up cycle.

The market price of chemical products is relatively stable. There were 12 kinds of products with rising prices in the chemical sector this week. The top 3 commodities were octanol (up 4.25% from the previous month, up 36.79% year-on-year, down 0.29 percentage points from last week) and pure benzene (1.31% increase from the previous month). It increased by 18.64% year-on-year and 2.90% lower than last week. Styrene (+2.9% increase, 18.97% year-on-year, 10.58% increase from last week). There were 11 kinds of products with a decrease in the chain, and the top 3 products were chloroform (down 4.76% from the previous month, up 48.24% from the previous year, down 8.27 percentage points from last week) and aniline (down 6.22% from the previous month and up 39.29% from the same period last year). Compared with last week, 10.8 percentage points and hydrochloric acid (down 3.31% from the previous month, down 33.19% from the same period of last year, up by 0.08 percentage points from last week).

3 , upstream: the dollar weakens, oil prices fall, and the color is stronger

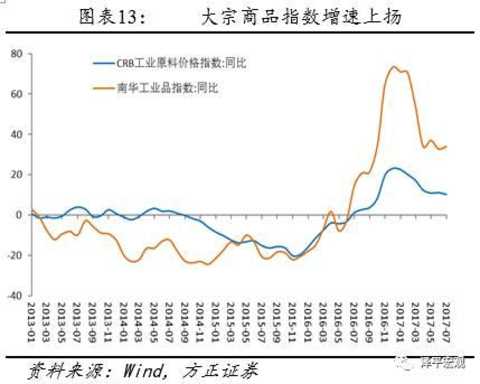

This week, the CRB industrial raw materials index increased by 0.54% from the previous month to 11.7% in August, up from 10.3% in July. SOUTH index industrial chain increased 0.43%, an 39.9% in August, 34.2% higher than an Jul; South China Agricultural 000061, stock index diagnosis chain increased 0.76%, up 2.2% in August, up 0.2% higher than in July.

The global central bank's annual meeting is about to strike, the market remains cautious, and the US dollar index is falling again. The US dollar index was weak this week, -0.24% from the previous month, and the US dollar index was -2.1% in August, down from -1.6% in July. The announcement of the minutes of the Fed meeting suppressed the market sentiment, and the situation of interest rate divergence was unclear. The Jackson Hall meeting kicked off on Thursday, when Federal Reserve Chairman Yellen and European Central Bank President Draghi will deliver a speech. On August 26, the US dollar fell again under pressure before the meeting. Affected by the fall in the US dollar and the impact of US economic data and the political situation on the Korean peninsula, gold prices climbed slightly. This week, London spot gold increased by 0.4% from the previous month, compared with -4.5% in August, up from -7.6% in July.

The oil market is still pessimistic due to oversupply concerns and the threat of a breach of the OPEC production cuts agreement. This week, Brent crude oil prices fell by -0.28% from the previous month and 8.2% year-on-year in August, up from 4.2% in July. US crude oil inventories fell for the eighth consecutive week last week, but as the joint technical committee of OPEC and non-OPEC oil producing countries met on Monday, there was no result, and the overall market atmosphere remained pessimistic. EIA crude oil inventories in the week of August 18 - 3.327 million barrels, the lowest level in a single week since October 2015, expected -34.58 million barrels; gasoline inventory -123,000 barrels, expected -100,000 barrels.

Non-ferrous metals have risen all round. The supply side capacity cleanup gradually landed, and the forecasting of production and the decline of inventory led to price increases. LME copper increased by 1.6% this week, compared with 34.6% in August, up from 23.1% in July. LME aluminum prices fell by 1.0% on a week-on-week basis, compared with 22.5% in August, up from 16.8% in July. LME zinc prices fell 0.1% on a week-on-week basis, compared with 28.9% in August, up from 27.5% in July.

4 , the price: the price of vegetables fell, the price of pigs rose

The average wholesale price of 28 key vegetables monitored by the Ministry of Agriculture decreased by 1.0% this week. The Qianhai Vegetable Wholesale Price Index decreased by 1.5% from the previous month. The influence of high temperature weather in Shandong on supply was weakened, and the vegetable wholesale price index decreased by 3.1%. The average wholesale price of 28 key vegetables for monitoring in the Ministry of Agriculture, the wholesale price index of Qianhai vegetables and the wholesale price index of vegetables in Shandong were 4.5%, 1.1% and 17.8%, respectively, higher than, lower than and lower than July. 2.8%, 2.7% 20.1%.

The average wholesale price of pork in the Ministry of Agriculture this week dropped by 0.2% from the previous month, and fell by 19.8% year-on-year in August, up from -22.8% in July. The average retail price of pork in 36 cities was unchanged from last week, down 10% year-on-year in August, up from -11.3% in July. The National Development and Reform Commission issued the "Analysis of the price of pigs in the first half of the year and the analysis of the later trend", warning that the supply of pork in the second half of the year may increase further, and the overall price of pigs will still decline. The average retail price of beef and mutton in 36 cities was -0.3% and -2.5% in August, respectively, higher than -1.0% and -2.8% in July. The average retail price of grass carp and carp in 36 cities was 9.6% and 3.9% respectively in August, down from 10.6% and 5.4% in July.

In terms of non-food, oil prices and drug prices both fell year on year. The growth rate of national refined oil prices continued to fall. July rose 5.2% year-on-year, slightly lower than 5.5% in June. China Chengdu Chinese herbal medicine price index.

5. Currency: stronger exchange rate, interest rates both long and short end liter

This week, the central bank's open market has a total of 750 billion reverse repurchase maturity, which expires 230 billion, 70 billion, 220 billion, 100 billion and 130 billion respectively from Monday to Friday. No repurchase and central bank bills expired.

Last Friday, the central bank carried out a 70 billion 7-day, 50 billion 14-day reverse repurchase operation, achieving a net investment of 20 billion yuan. On Monday, the central bank opened up the market for 100 billion 7 days, 80 billion 14 days reverse repurchase operations, and realized a net return of 50 billion yuan. On Tuesday, 40 billion 7 days, 20 billion 14 days reverse repurchase operations, a small net return of 10 billion yuan. On Wednesday, the central bank opened up the market for 100 billion 7 days, 80 billion 14 days of reverse repurchase operations, and net withdrawal of 40 billion. On Thursday, the central bank did not carry out reverse repurchase operations, and realized a net return of 100 billion yuan on the same day.

This week, the central bank continued to “cut the peak†due to the impact of fiscal expenditure at the end of the month. At the end of the month, the fiscal expenditure can hedge the central bank’s reverse repurchase maturity and other factors. In order to maintain the basic stability of liquidity and maintain the monetary policy of the stable center, the central bank has four consecutive years. The day maintains a net return. At the same time, the long-awaited special government bonds have continued to fall. The Ministry of Finance announced that the first phase of the 600 billion yuan special national debt in 2007 will be due to expire on August 29, and will start the cash buyout tool to buy the 600 billion yuan from the financial institutions through the bond secondary market. The yuan special treasury bond, the release model once again shows the central bank's stable neutral monetary policy.

As of August 24, the 1-day inter-bank repurchase plus rights ratio was 3.0584%, up 6.76 BP from last week; the 7-day inter-bank repurchase plus rights ratio was 3.8028%, up 27.54 BP from last week. The 1-day deposit-type institutions repurchased and added rights ratio was 2.8711%, up 2.94 BP from last week; the 7-day deposit-type institutions repurchased plus rights ratio was 2.9104%, up 3.91 BP from last week. The one-year government bond yield was 3.3355%, down 0.18 BP from last week; the 10-year government bond yield was 3.6152%, up 2.01 BP from last week.

The direct interest rate (monthly interest rate) of the Pearl River Delta Bill, the direct interest rate of the Yangtze River Delta Notes (monthly interest rate) and the interest rate of the bill transfer (monthly interest rate) were all the same as last week. Credit differentials for different maturities this week, the credit spread of 1-year AAA corporate bonds increased by 6.66 BP, and the credit spread of 10-year AAA corporate bonds narrowed by 1.93 BP.

The US dollar index was weak and the RMB exchange rate rose. This week, the central parity of the US dollar against the RMB depreciated by 0.17%, the US dollar against the RMB spot exchange rate depreciated by 0.22%, and the offshore RMB appreciated by 0.28%. The onshore and offshore RMB exchange rate spreads increased from -0.0033 last week to 0.0002. The US dollar against the RMB 1-year foreign exchange forward purchase price fell by 15 BP, and the RMB forward depreciation pressure decreased.

Indoor outdoor rugs with tassels

Indoor Outdoor Rugs With Tassels,Indoor Outdoor Carpet Lowe'S,Indoor Outdoor Door Mats,Shaw Indoor Outdoor Carpet

Hengshui Namei Imp.&Exp. Co.,Ltd. , https://www.nameirug.com